Intro

Securian SecureCare, introduced in 2017, was one of the first hybrid policies to offer 100% cash benefits directly to policyholders, giving them unmatched flexibility when it matters most.

This individual hybrid policy might not have the spotlight like Nationwide's CareMatters policies, but it doesn’t need flashy TV ads to shine. Backed by Securian Financial, one of the highest-rated insurance companies on the planet, it delivers:

- Top benefit pools: Get access to more funds for care costs.

- Cash indemnity: Spend your benefits however you see fit.

- Good tax savings: Lower your overall policy costs.

SecureCare III is like Dana Scully from The X-Files—under the radar, offering immense value without fanfare. Scully is the one exposing a government conspiracy to hide the truth of alien colonization without Mulder’s theatrics.

If you didn't watch The X-Files, here's a 30-second clip where Scully demonstrates her gun-grabbing ninja skills.

As you consider your options, let “LTC” guide you: Learn about the choices available, Talk openly with family, and Create a plan that supports your shared future. SecureCare III might be the linchpin of your plan, bringing underrated value that outshines its more attention-grabbing peers.

Post jargon

benefit: the amount LTCi pays for covered care expenses

benefit period: the maximum time LTCi pays for care after criteria are met

benefit pool: total amount available in LTCi for care expenses

cash indemnity: pays the full benefit, regardless of the actual care costs

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

elimination period: the waiting period after criteria are met before benefits start

exclusion: an insurance rule that denies benefits for specific risks

inflation protection: LTCi benefit that adjusts for rising costs

premium: the payment to maintain insurance

rider: an insurance add-on

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

Standard benefits

SecureCare comes with many standard benefits of a hybrid policy:

- Guaranteed premiums: Your costs can never...go...up.

- Guaranteed benefits: Your payouts always match your policy terms.

- Benefit triggers: Coverage starts when you need help with two ADLs or cognitive decline.

- Broad coverage: Includes informal care (e.g., family), home health care, adult day care, assisted living, nursing homes, memory care, CCRCs, care coordination, respite care, and hospice.

- Inflation protection (optional): Keeps your benefits aligned with rising costs.

- Death benefit: If you never use your benefits, your family receives a payout upon your death.

- Money-back option: Cancel your policy anytime and get some or all of your money back.

What's special about SecureCare?

In a competitive market, policies often include standout features to set themselves apart. Let’s take a closer look at what makes SecureCare special.

Top benefit pools

A benefit pool is the total amount available to cover long-term care expenses, whether for home care, assisted living, or other support. This policy offers one of the largest benefit pools on the market, delivering more value for your premium dollar. At the bottom of this post, you'll find a comparison table showing how it stacks up against other policies.

Cash indemnity

This policy offers cash indemnity payouts, providing higher payouts and greater flexibility compared to traditional reimbursement-based policies.

- No need to submit receipts – less paperwork, less hassle.

- Full, maximum benefit – paid each month, regardless of actual care costs.

- Freedom to spend on any type of care – including payments to family caregivers, with fewer exclusions and no approvals required.

Good tax savings

In many cases, you can deduct the LTCi portion of your premium, but not the life insurance portion. SecureCare III separates these premiums, allowing you to take this deduction.

The details

If this policy sounds intriguing, we'll get you answers to your questions.

We rate each policy’s benefits, premiums, underwriting, and company on a three-star scale, with three stars being the best.

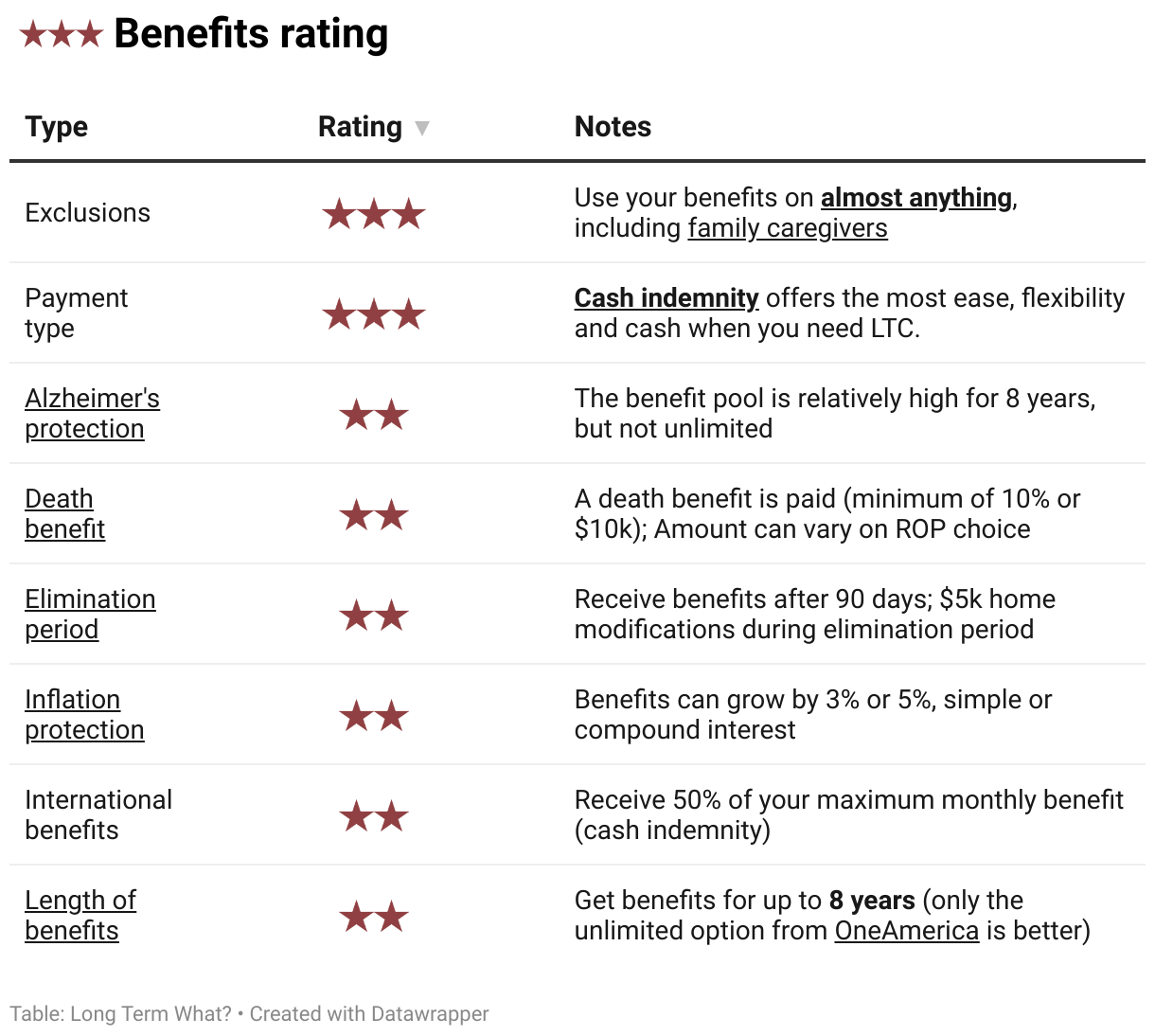

Benefits

Premiums are the payments made to maintain insurance.

SecureCare III often provides the highest, most flexible benefits of any hybrid policy.

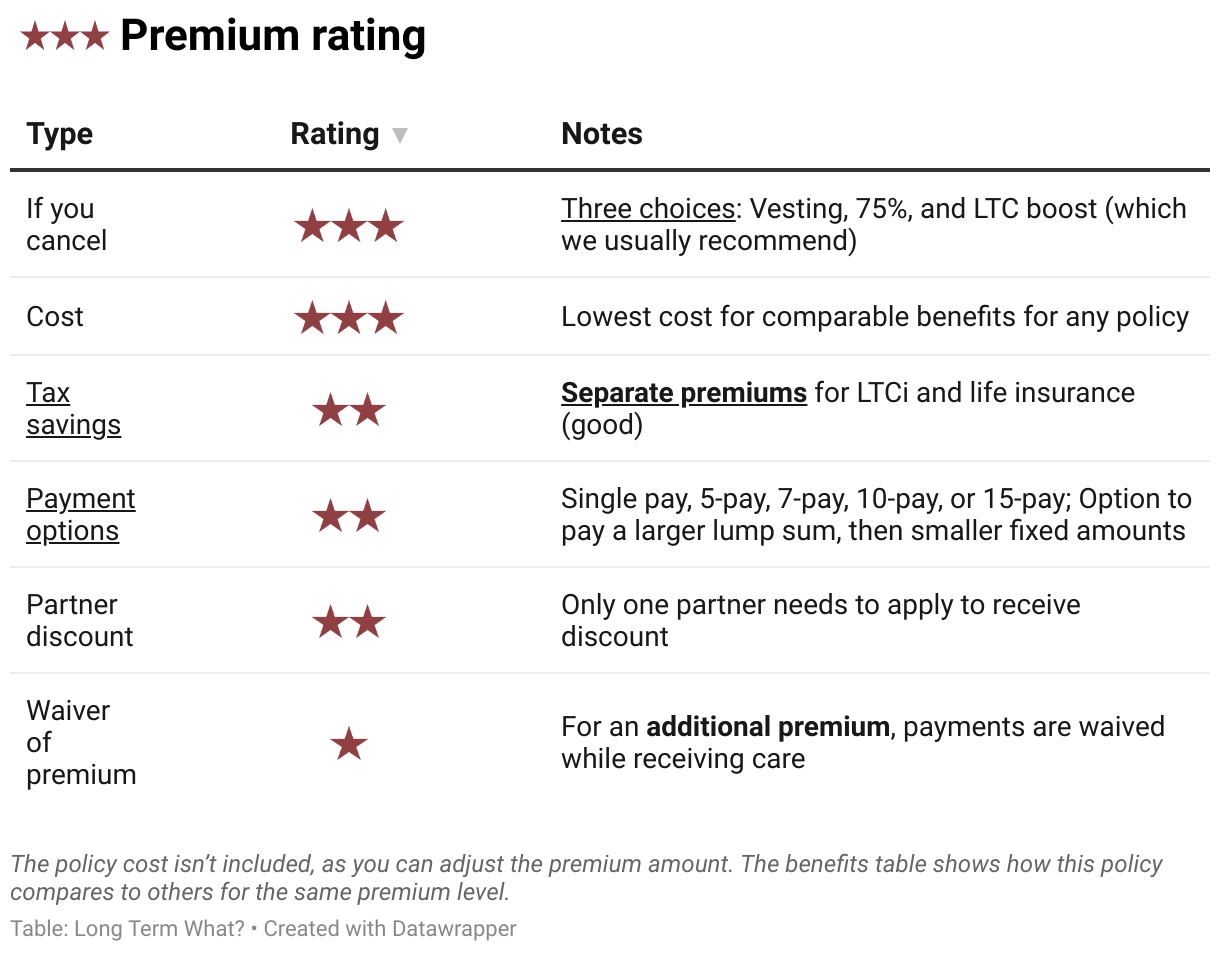

Premium

Premiums are what you pay for insurance coverage.

SecureCare offers guaranteed premiums that will never increase, along with a variety of flexible premium options.

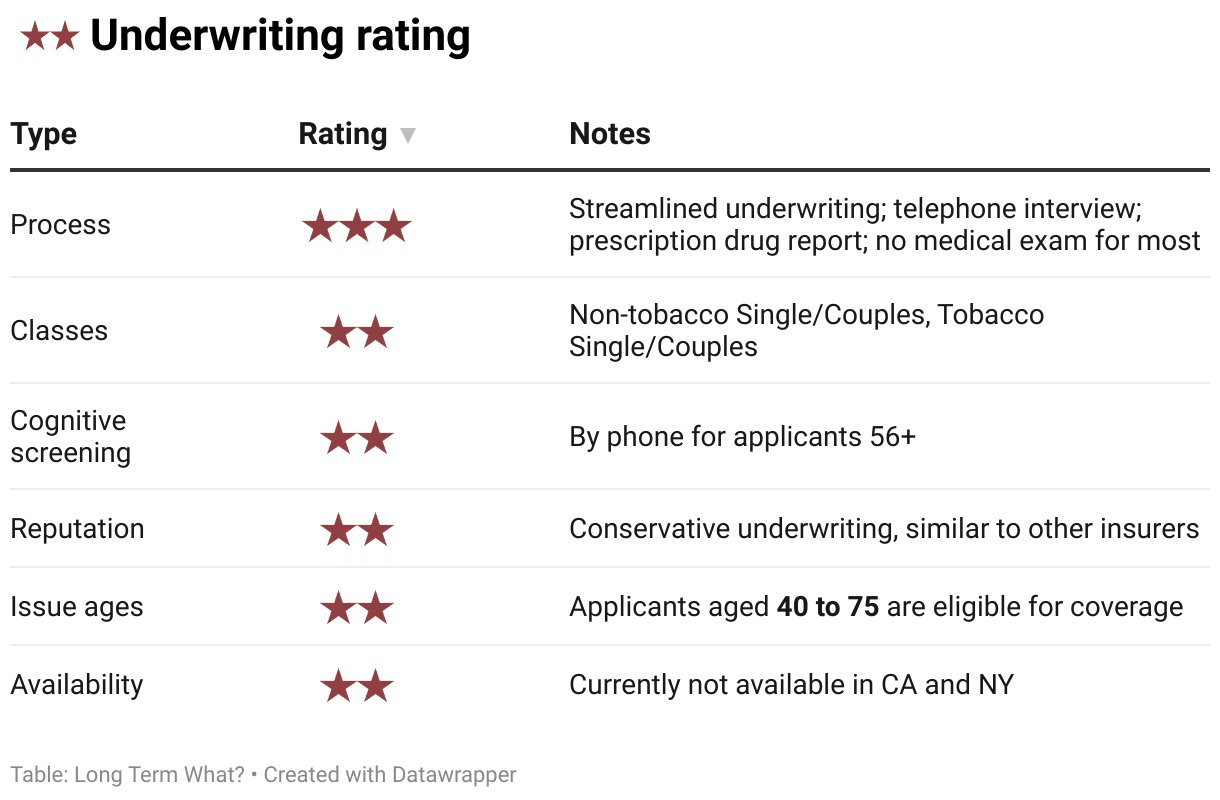

Underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

Securian provides fairly standard underwriting compared to other policies we offer.

Company

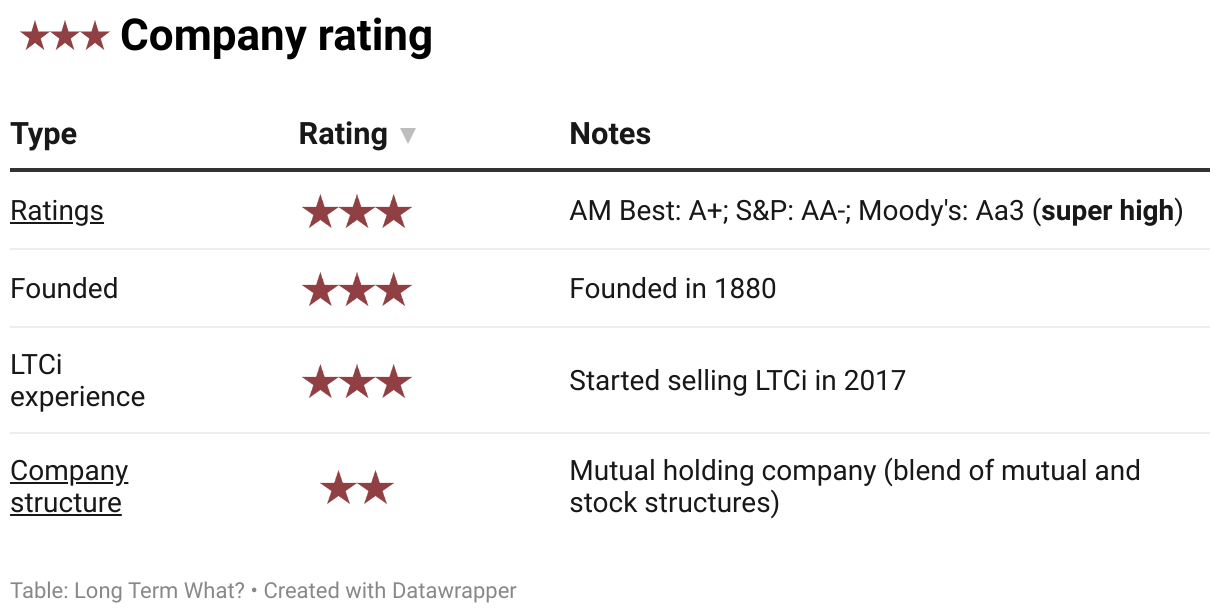

Choose a top-rated insurer for reliable LTC coverage. We work only with financially strong companies to ensure they’ll be there when it counts.

The SecureCare III policy is issued by Minnesota Life Insurance Company (Securian Life in New York). Both are subsidiaries of Securian Financial Group, Inc. All of these companies have almost identical, super-strong ratings.

Comparisons

How does SecureCare III compare to other LTCi policies? Focus on what matters most to you to make the best policy choice.

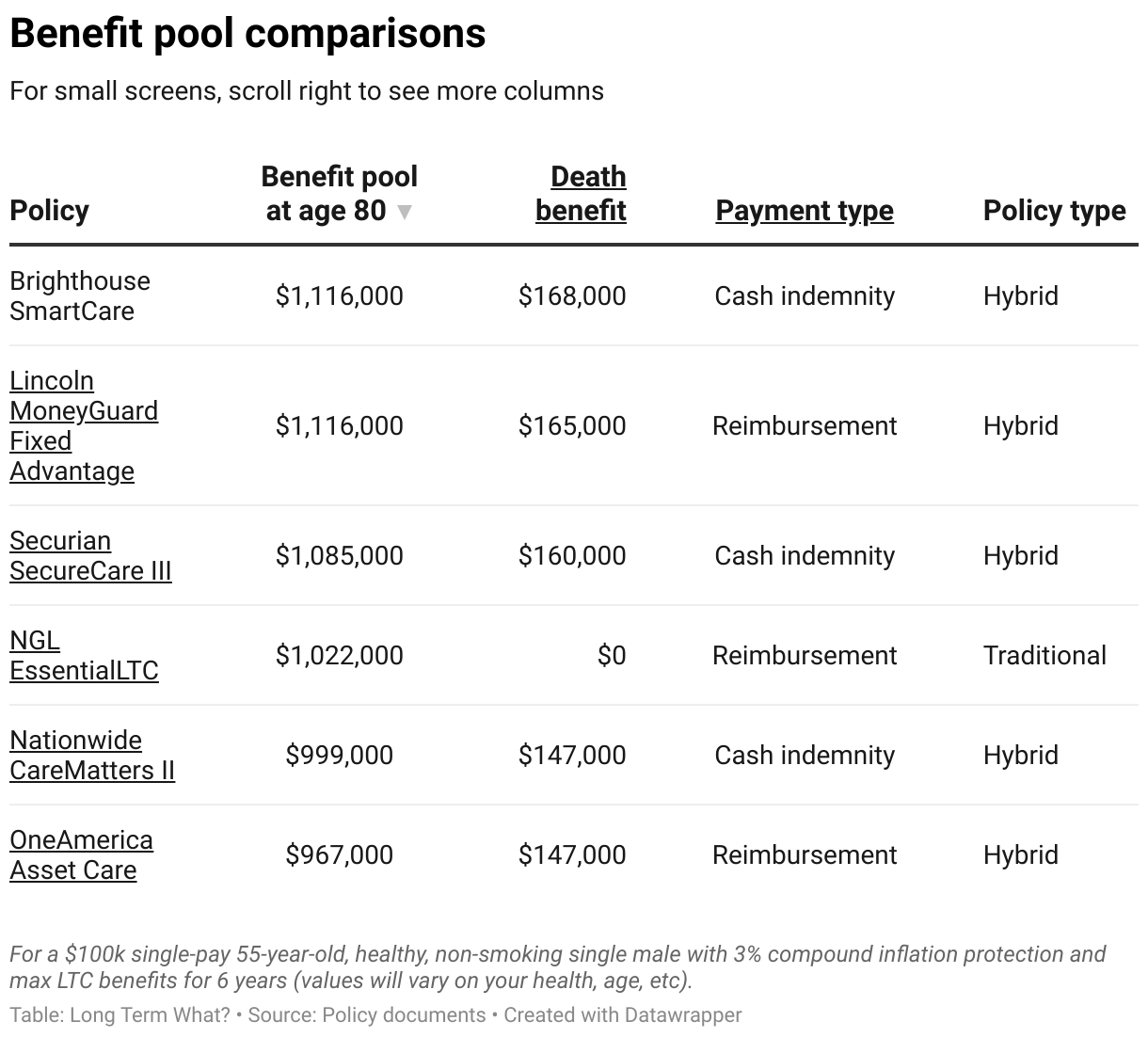

Benefit pools

Compare the benefit pools offered by different individual policies for the same premium.

Benefits

In this table, you can compare the benefits of all the LTCi policies we offer. You can:

- Search for any detail.

- Tap any column title to sort.

- Scroll right to view more columns. ➡️

Next steps

If this policy seems like a good fit, click the button below and include 'SecureCare' in the notes section at the final step.

Wrap up

Just like Dana Scully’s steady, underappreciated work in The X-Files, SecureCare III is an unsung hero in the world of hybrid long-term care policies.

This policy could be an ideal fit if you’re looking for:

- Cash indemnity benefits that give you control over how you use your LTC funds

- One of the highest pools of LTC benefits among hybrid policies

- Tax advantages, especially for small business owners

- Rock-solid financial backing from a highly rated company

With its unique flexibility and substantial benefits, SecureCare III may just be the linchpin of your long-term care plan.