Intro

Asset Care is one of the first hybrid long-term care insurance (LTCi) policies, first introduced over 30 years ago. As the only hybrid plan offering lifetime benefits, Asset Care ensures you’re prepared for extended memory care costs, one of the most unpredictable and expensive aspects of long-term care.

Asset Care offers a number of special benefits:

- Lifetime benefits: Coverage for extended memory care costs.

- Joint policy: Lower costs for two people under one plan.

- Cash indemnity...kinda: Some cash benefits for the first two years.

- Great care coordination: Get more TLC for LTC.

- Tax breaks: Lower your overall policy costs.

- Pay with qualified funds: Use retirement funds for premiums.

If we had to compare Asset Care to a fictional battery-powered animal that appeared in commercials in the 80s, it’d be the Energizer Bunny. This policy's lifetime benefits are built for longevity—famously "going and going" no matter what.

For a trip down memory lane, here’s a 30-second clip of two classic Energizer Bunny ads, including one where you can order things on the Internet. 🤯

As you consider your options, let "LTC" guide you: Learn about options, Talk with family, and Create a plan that supports your shared future. If you want to insure for the costs of Alzheimer's care, this policy should be considered in your plan.

Post jargon

benefit: the amount LTCi pays for covered care expenses

benefit period: the maximum time LTCi pays for care after criteria are met

benefit pool: total amount available in LTCi for care expenses

cash indemnity: pays the full benefit, regardless of the actual care costs

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

elimination period: the waiting period after criteria are met before benefits start

exclusion: an insurance rule that denies benefits for specific risks

inflation protection: LTCi benefit that adjusts for rising costs

premium: the payment to maintain insurance

rider: an insurance add-on

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

Standard benefits

Asset Care comes with many standard benefits of a hybrid policy:

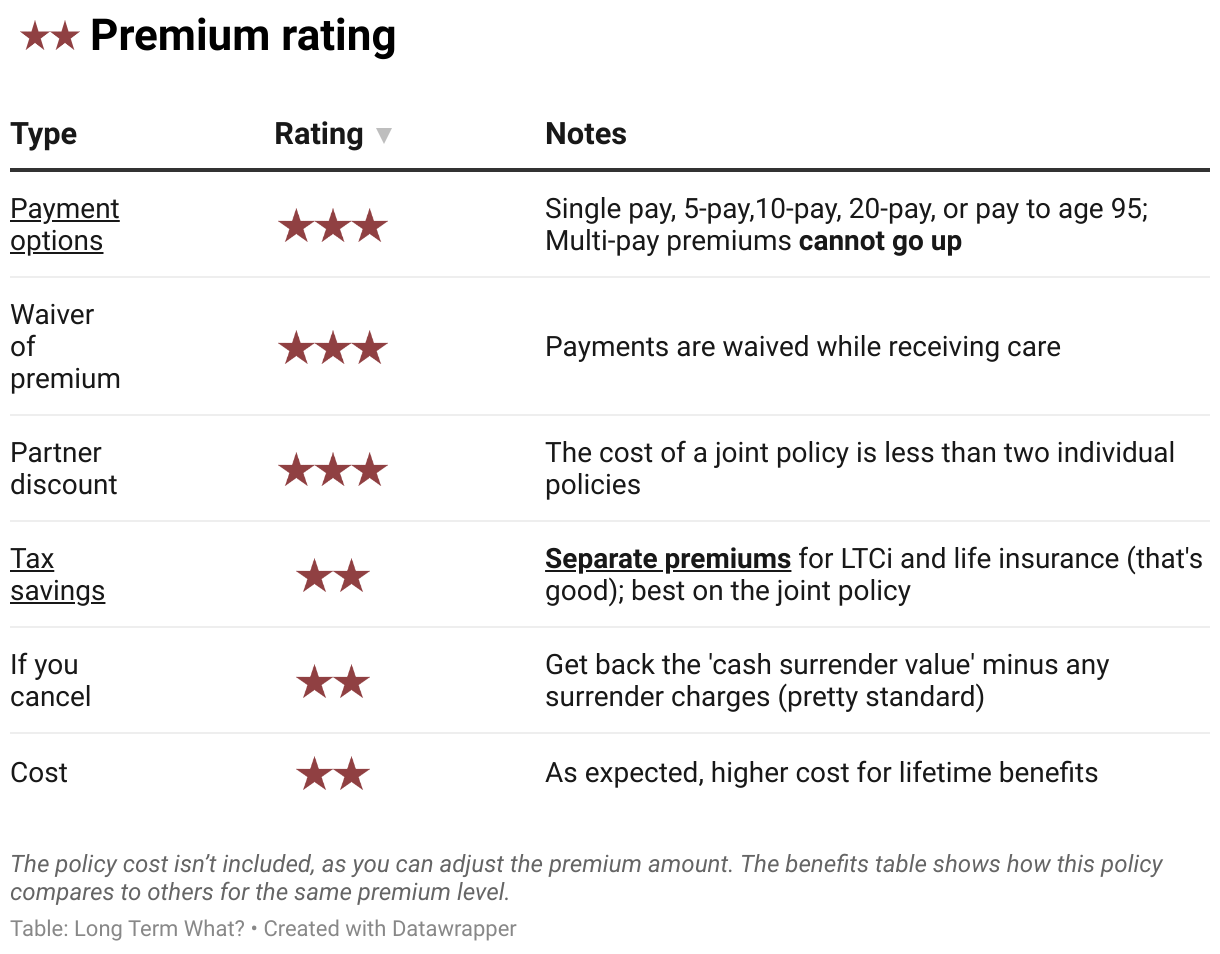

- Guaranteed premiums: Your costs can never...go...up.

- Guaranteed benefits: Your payouts always match your policy terms.

- Benefit triggers: Coverage starts when you need help with two ADLs or cognitive decline.

- Broad coverage: Includes limited informal care (e.g., family), home health care, adult day care, assisted living, nursing homes, memory care, CCRCs, care coordination, respite care, and hospice.

- Inflation protection (optional): Keeps your benefits aligned with rising costs.

- Death benefit: If you never use your benefits, your family receives a payout upon your death.

- Money-back option: Cancel your policy anytime and get some or all of your money back.

What's special about Asset Care?

In a competitive market, policies often include standout features to set themselves apart. Let’s take a closer look at what makes Asset Care special.

Lifetime benefits

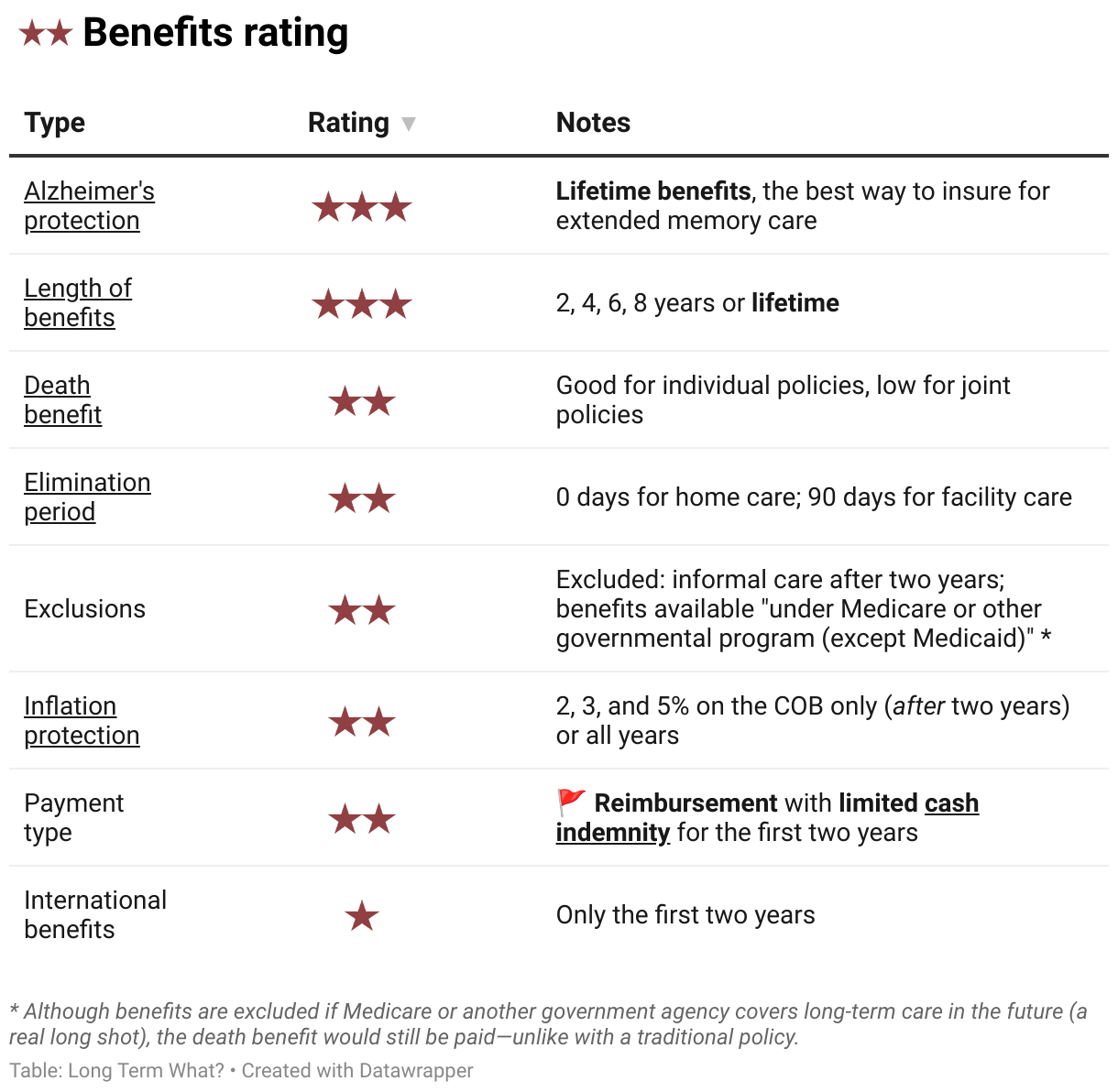

Asset care is the only hybrid policy to offer lifetime benefits.

Yep, this one is a doozie.

Most policies limit the benefit period to 6 to 8 years, but Asset Care coverage keeps going and going. For your lifetime.

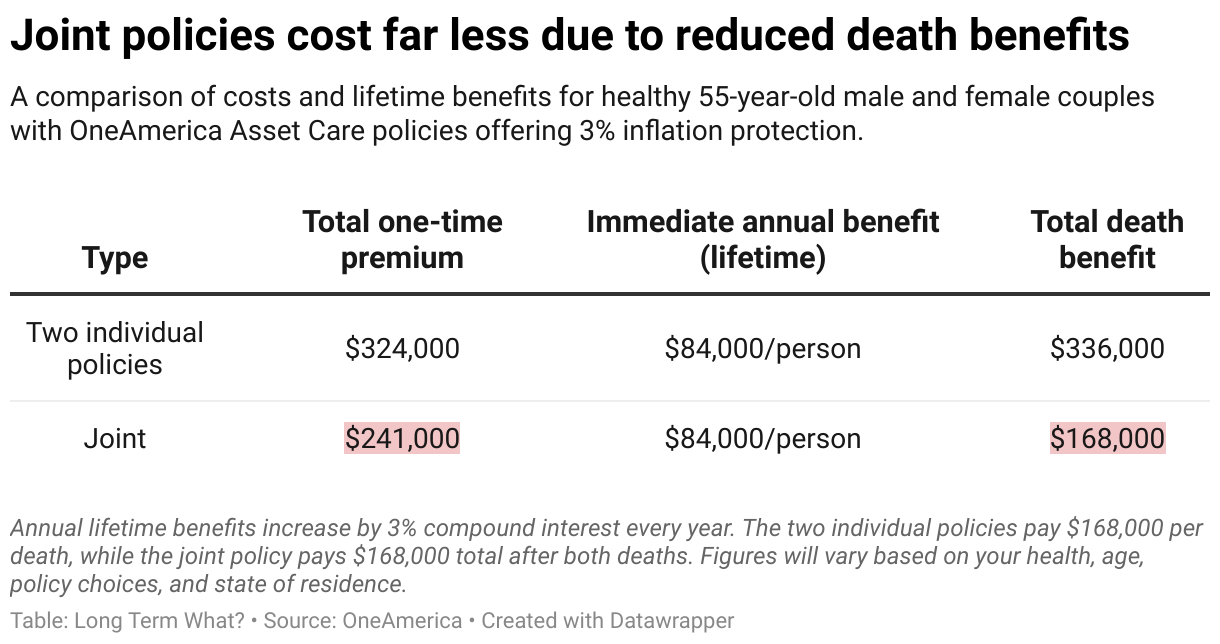

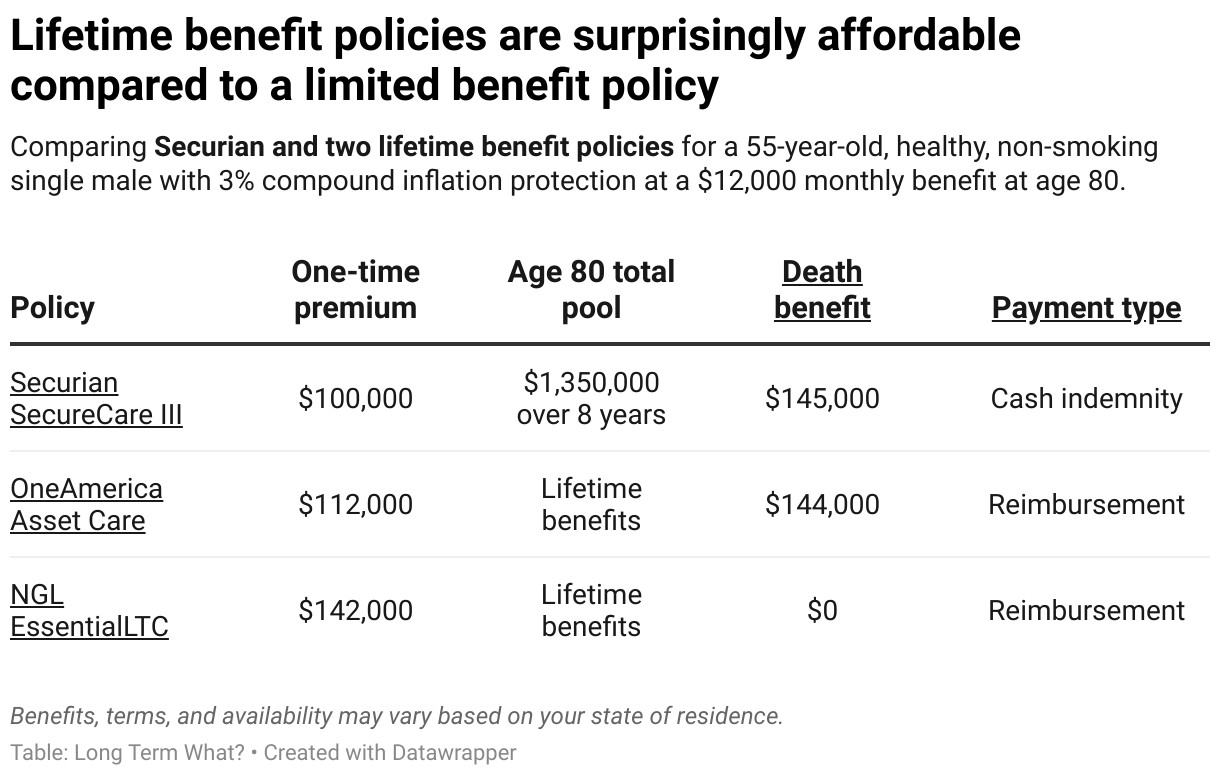

It’s important to weigh the cost of lifetime benefits, but it might be more affordable than you’d think—especially if you get a joint policy. See the bottom of this post for policy comparisons.

Joint policy

You can purchase Asset Care as an individual or joint policy. The only other joint hybrid option on the market is CareMatters Together.

A joint policy differs from buying two individual policies in a few ways:

- Increased LTC coverage: A larger portion of the benefits is allocated to LTCi compared to life insurance.

- More tax benefits: A larger percentage of the premium goes toward LTC coverage, which may provide additional tax advantages.

- Delayed death benefit: Unlike individual policies, where the surviving partner receives the death benefit when the first partner passes, joint policies delay the death benefit payout until both partners have passed.

- Lower overall cost: If your priority is LTCi benefits, joint policies offer a significantly more affordable option compared to buying two individual policies.

Cash indemnity... kinda

Asset Care primarily offers reimbursement payouts for benefits.

But in 2024, they added a limited cash indemnity benefit with these caveats:

- Only available for the first two years of care

- Up to 75% of your monthly benefit limit (not the full 100%)

Cash indemnity payouts provide higher payouts and greater flexibility compared to reimbursement.

- No need to submit receipts – less paperwork, less hassle.

- Full 75% benefit – paid each month, regardless of actual care costs.

- Freedom to spend on any type of care – including payments to family caregivers, with fewer exclusions and no approvals required.

This benefit was introduced to provide compensation for a family member or neighbor offering care during the initial stages, giving families valuable time to arrange more formal care options.

Since informal caregiving can often lead to burnout, the two-year limit strikes a practical balance—offering flexibility and relief while transitioning to professional in-home care or assisted living arrangements.

After two years, the policy only pays via reimbursement for formal providers.

Great care coordination

Most LTCi policies include some level of care coordination to support you when you need LTC, but One America has picked this area to shine.

Their concierge team consists entirely of in-house employees based in Indianapolis, rather than using third-party vendors. Their team offers:

- Care Benefit Concierge – A dedicated claims specialist to guide you through the claims process.

- Care Coordinator – Assistance in finding local facilities and providers tailored to your needs.

- Caregiver Consultant – A free monthly coach, available virtually or in person, to support informal caregivers at home.

Collectively, you'll feel the TLC for when LTC is needed. ❤️

Tax breaks

In many cases, you can deduct the LTCi portion of your premium, but not the life insurance portion. Asset Care separates these premiums, allowing you to take this deduction.

Pay with qualified funds

If you have qualified retirement funds like an IRA or 401(k), OneAmerica makes it simple to leverage them to buy LTCi and maximize your care options.

The details

If this policy sounds intriguing, let’s dive deeper.

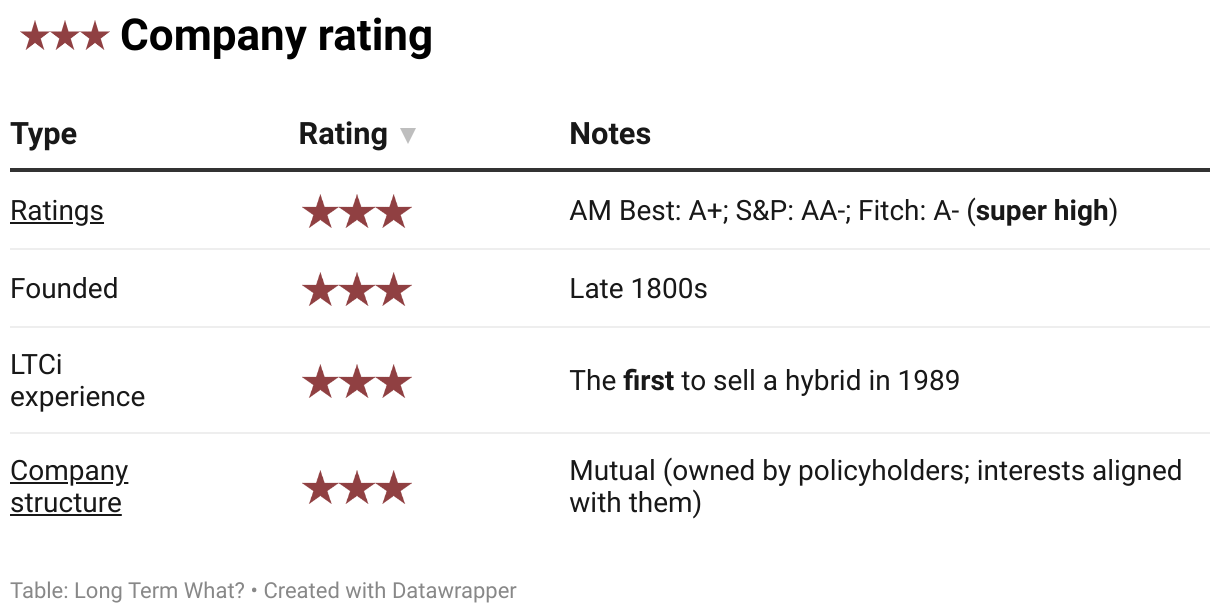

We rate each policy’s benefits, premiums, underwriting, and company on a three-star scale, with three stars being the best.

Benefits

Benefits are what the policy pays for covered care expenses.

Asset Care provides a unique solution to receive lifetime benefits and a death benefit.

Premium

Premiums are the payments made to maintain insurance coverage.

This policy provides a cost-effective option to cover two people with a joint policy, allows easy payment using qualified funds, and features guaranteed premiums that won’t increase.

Underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

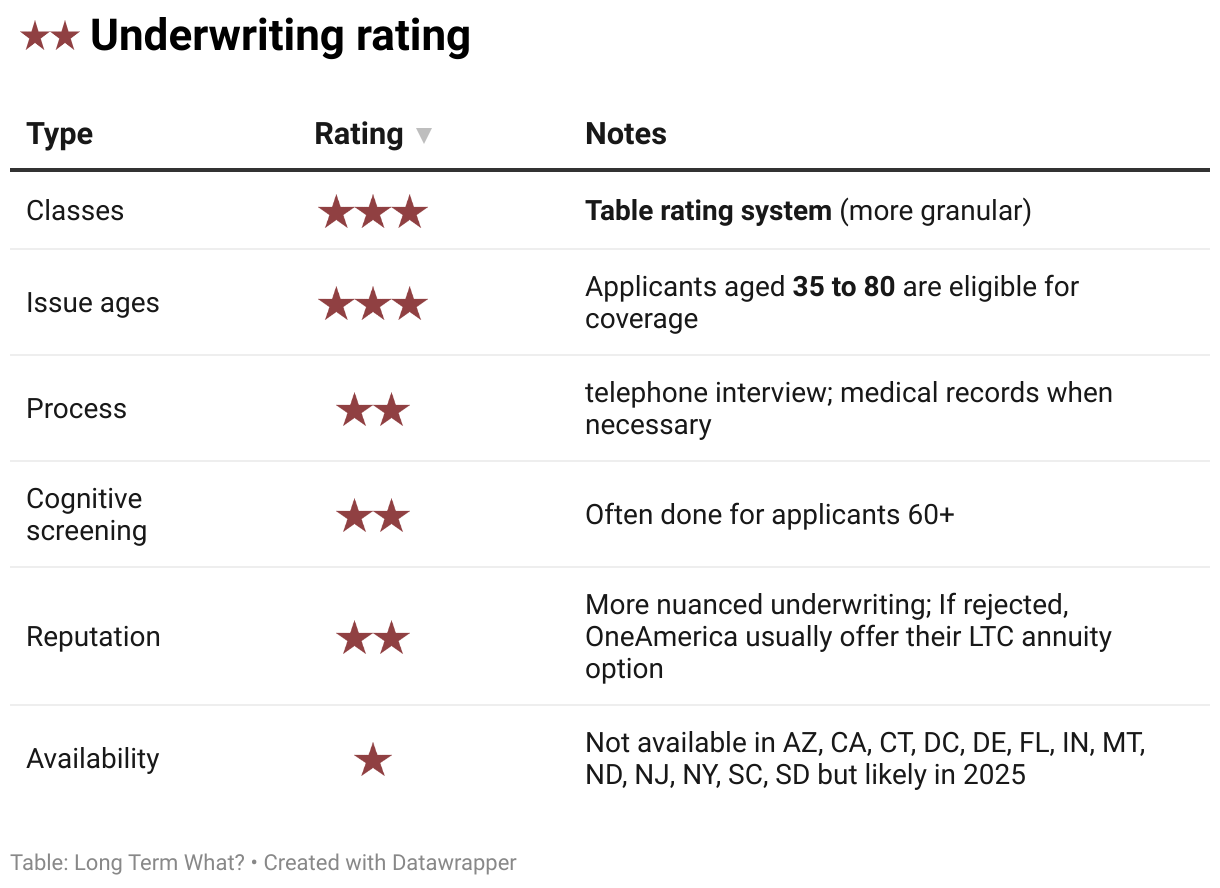

OneAmerica employs a table rating system that offers more granularity than traditional broad categories like standard, substandard, or decline. Health risks are assigned to specific tiers, with higher-risk individuals incurring proportionally higher costs.

Company

Choose a top-rated insurer for reliable LTC coverage. We work only with financially strong companies to ensure they’ll be there when it counts.

OneAmerica is a well-established company with roots dating back to before the advent of cars. In 1989, they introduced the first hybrid long-term care insurance policy. Asset Care is technically issued and underwritten by The State Life Insurance Company, a subsidiary of OneAmerica.

Comparisons

How does Asset Care compare with other LTCi policies? Focus on what matters most to you to make the best policy choice.

Extended care

Asset Care is a solid option for covering memory care costs, which can extend 8–10+ years. Compare this policy with other LTCi options to see how it measures up.

Benefits

In this table, you can compare the benefits of all the LTCi policies we offer. You can:

- Search for any detail.

- Tap any column title to sort.

- Scroll right to view more columns. ➡️

Next steps

If this policy seems like a good fit, take the quiz below and include 'Asset Care' in the notes section at the final step.

Wrap up

Like the Energizer Bunny, Asset Care keeps going and going, providing protection from the unexpected costs that come with long-term care. With Alzheimer’s care that can last 10-20 years, its unlimited benefits are built to handle this significant risk. Add in the death benefit and joint policy option, and it’s a plan worth considering.

However, you’ll need to weigh these upsides against the less flexible reimbursement policy and the overall cost. Be sure to get multiple quotes to compare and ensure this option fits your needs and budget—so you’re ready for whatever the future brings.