Intro

Lincoln Moneyguard is one of the first hybrid long-term care insurance (LTCi) policies, first introduced in 1987.

The newest version of the policy was released in 2024 offers some enticing benefits:

- High benefit pool: Get access to more funds for care costs.

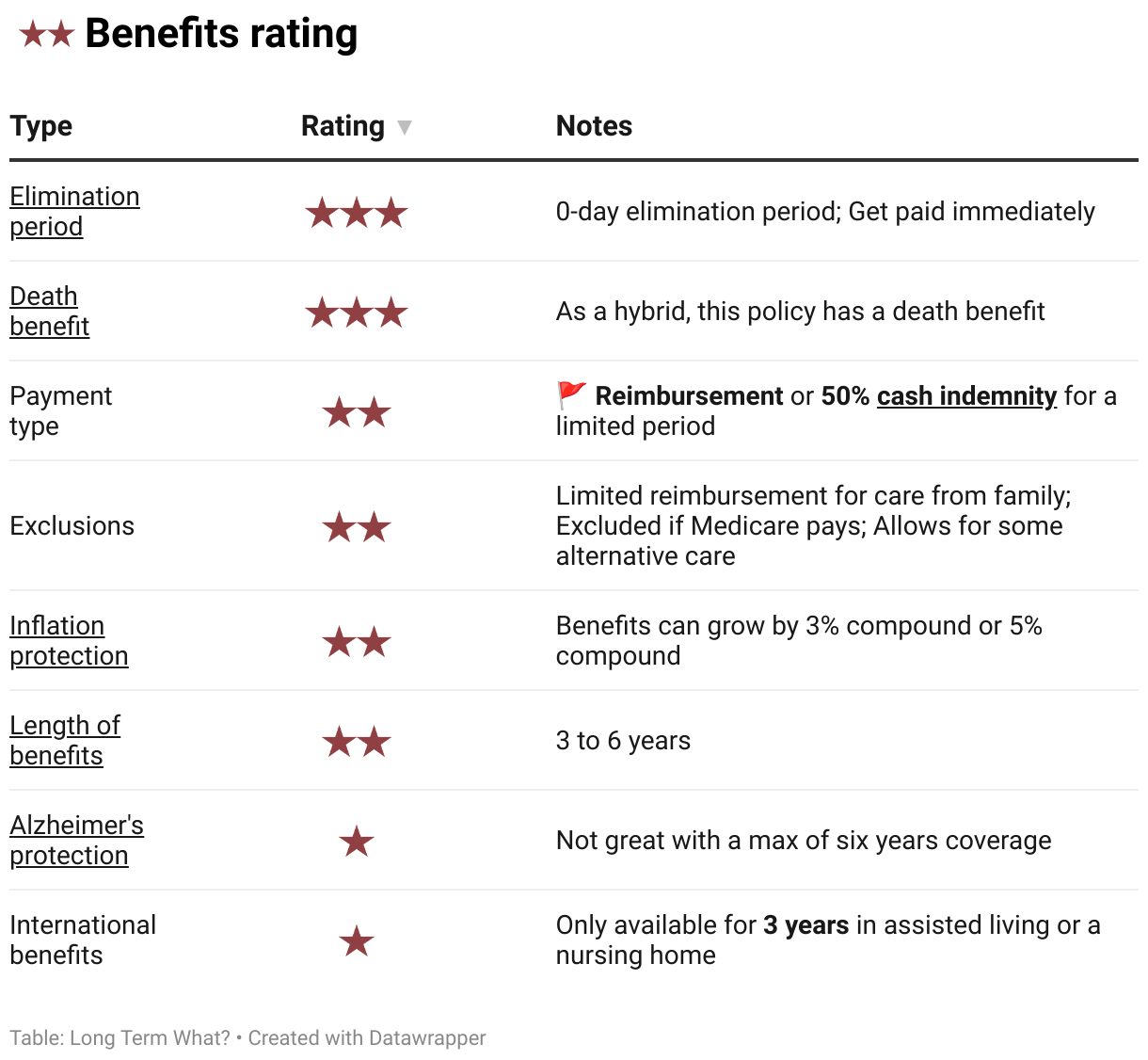

- Zero-day elimination period: Get paid for care from day one.

- A little cash indemnity: Some cash benefits for a limited time.

- Benefit transfer rider: Give your partner more benefits.

If we had to compare this policy to a timeless musical artist, it would be Stevie Nicks and Fleetwood Mac. Just as Fleetwood Mac dominated the 1970s, MoneyGuard was an early leader in hybrid LTCi policies. Although it faded from the spotlight in recent years, much like Nicks' quieter solo era, both are now making a strong comeback.

Enjoy this 30-second clip of the timeless classic, Landslide, performed in 1975.

As you consider your options, let "LTC" guide you: Learn about options, Talk with family, and Create a plan that supports your shared future. In the end, isn’t it all about harmonizing your decisions, like a timeless melody?

Post jargon

benefit: the amount LTCi pays for covered care expenses

benefit period: the maximum time LTCi pays for care after criteria are met

benefit pool: total amount available in LTCi for care expenses

cash indemnity: pays the full benefit, regardless of the actual care costs

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

elimination period: the waiting period after criteria are met before benefits start

exclusion: an insurance rule that denies benefits for specific risks

inflation protection: LTCi benefit that adjusts for rising costs

premium: the payment to maintain insurance

rider: an insurance add-on

specified amount: initial pool of money allocated for LTC or death benefits (same as face amount)

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

Standard benefits

MoneyGuard also with many standard benefits of a hybrid policy:

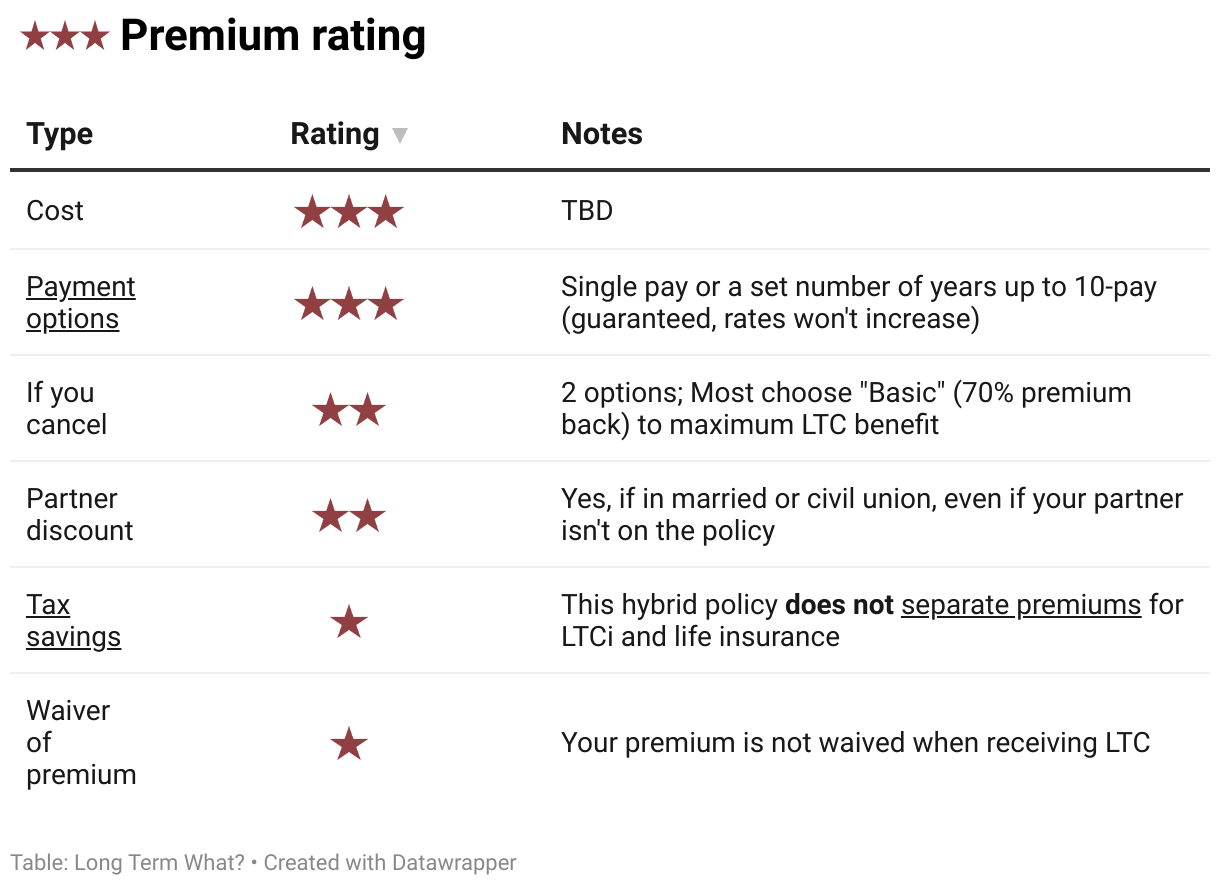

- Guaranteed premiums: Your costs can never...go...up.

- Guaranteed benefits: Your payouts always match your policy terms.

- Benefit triggers: Coverage starts when you need help with two ADLs or cognitive decline.

- Broad coverage: Includes informal care (e.g., family), home health care, adult day care, assisted living, nursing homes, memory care, CCRCs, care coordination, respite care, and hospice.

- Inflation protection (optional): Keeps your benefits aligned with rising costs.

- Death benefit: If you never use your benefits, your family receives a payout upon your death.

- Money-back option: Cancel your policy anytime and get some or all of your money back.

What's special about MoneyGuard?

In a competitive market, policies often include standout features to set themselves apart. Let’s take a closer look at what makes Lincoln MoneyGuard special.

High benefit pool

In early 2024, Lincoln raised their benefit game to be more competitive in the marketplace.

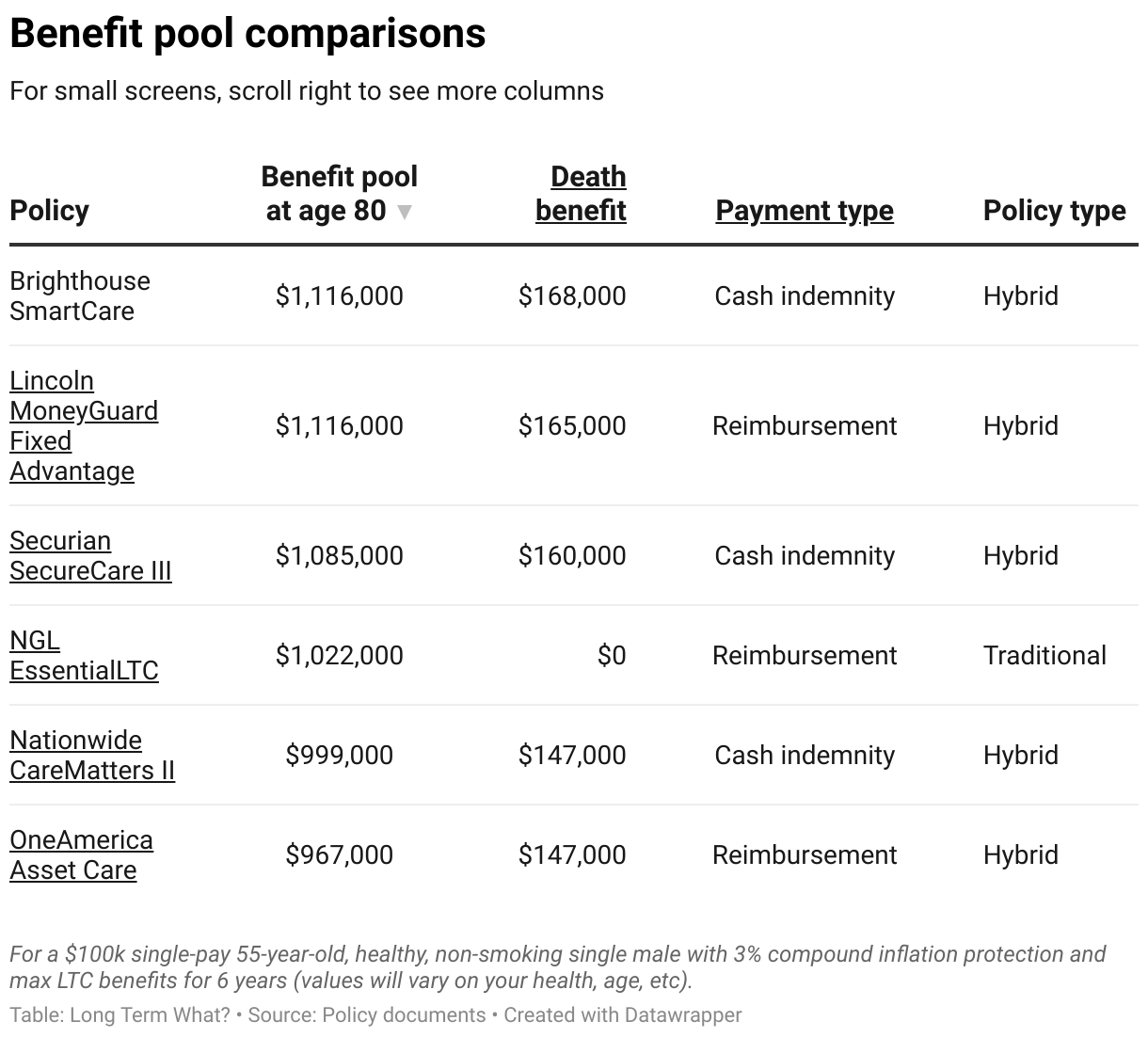

A benefit pool is the total amount available to cover long-term care expenses, whether for home care, assisted living, or nursing care.

This policy offers one of the largest benefit pools on the market, delivering more value for your premium dollar. At the bottom of this post, you'll find a comparison table showing how it stacks up against other policies.

Zero-day elimination period

An elimination period, or waiting period, is the time after you qualify for benefits during which you must pay care costs out of pocket before your policy starts paying.

Most long-term care policies include a 90-day elimination period. This particular policy stands out by offering a zero-day elimination period, meaning you'll receive benefits immediately when you need care.

A little cash indemnity

Lincoln MoneyGuard primarily offers reimbursement payouts for benefits.

But in 2024, they added a limited cash indemnity benefit with a few conditions:

- Available for a limited period of time (once your specified amount is used up)

- Up to 50% of your monthly benefit limit (not the full amount)

Cash indemnity payouts provide higher payouts and greater flexibility compared to reimbursement.

- No need to submit receipts – less paperwork, less hassle.

- Full, maximum benefit – paid each month, regardless of actual care costs.

- Freedom to spend on any type of care – including payments to family caregivers, with fewer exclusions and no approvals required.

This benefit was designed to compensate family members or neighbors who provide care during the early stages of a care need. It gives families valuable time to arrange more formal care options.

Since informal caregiving can often lead to burnout, the limited cash indemnity benefit strikes a practical balance. It offers flexibility and short-term relief while helping families transition to professional in-home care or assisted living.

Benefit transfer rider

Lincoln MoneyGuard offers a benefit transfer rider at no extra cost.

If you pass away with a remaining death benefit, your beneficiary can use that amount to purchase additional coverage on their own MoneyGuard policy without the need for underwriting.

- What doesn’t change: Their monthly benefit remains the same.

- What does change: Their total pool of money increases with some leverage, extending the benefit period (e.g., from 6 years to 7 years).

While this means more money overall, the funds are harder to access because they’re tacked onto the end of their benefit period, rather than being available upfront.

The details

If this policy piques your interest, we’ll hit all the right notes to uncover the key details that matter.

We rate each policy’s benefits, premiums, underwriting, and company on a three-star scale, with three stars being the best.

Benefits

Benefits are what the policy pays for covered care expenses.

MoneyGuard offers a large benefit pool and a zero-day elimination period, but its reimbursement payments are less flexible.

Premium

Premiums are the payments made to maintain insurance coverage.

MoneyGuard premiums are guaranteed never to increase, while its other features are fairly standard.

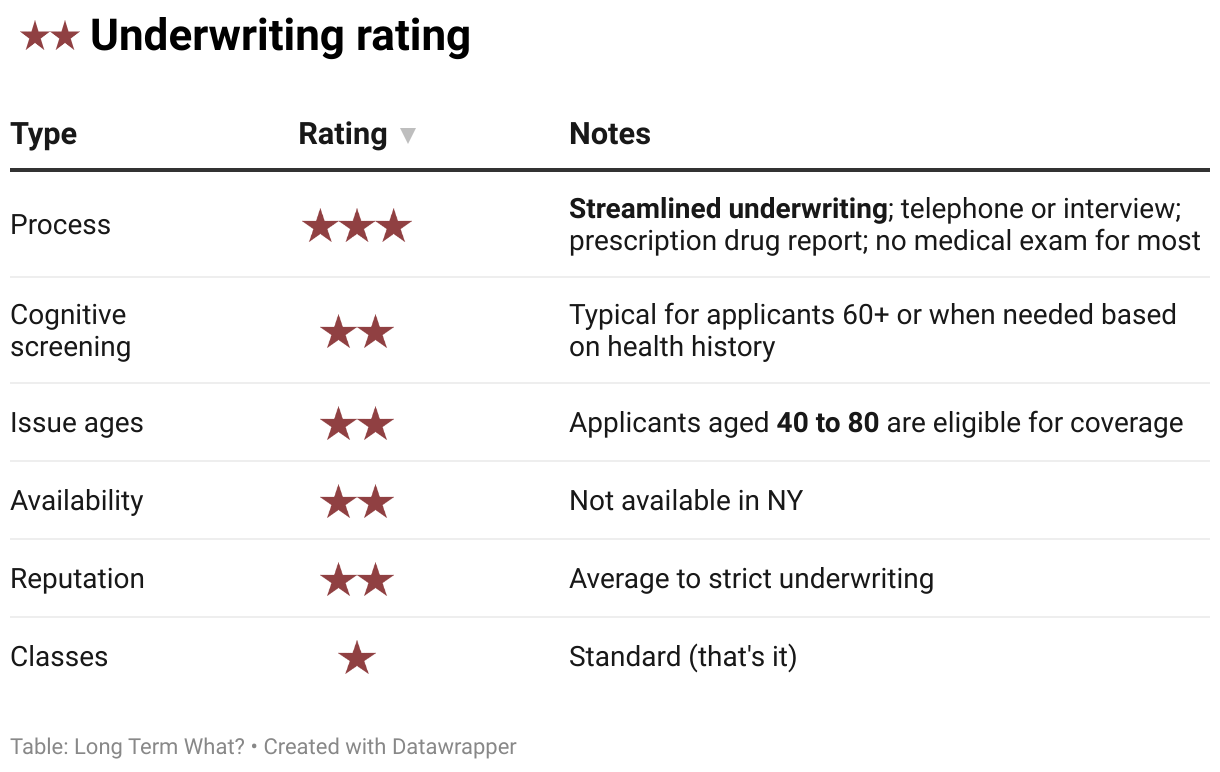

Underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

Lincoln offers a widely available policy with streamlined underwriting, providing quick approval times.

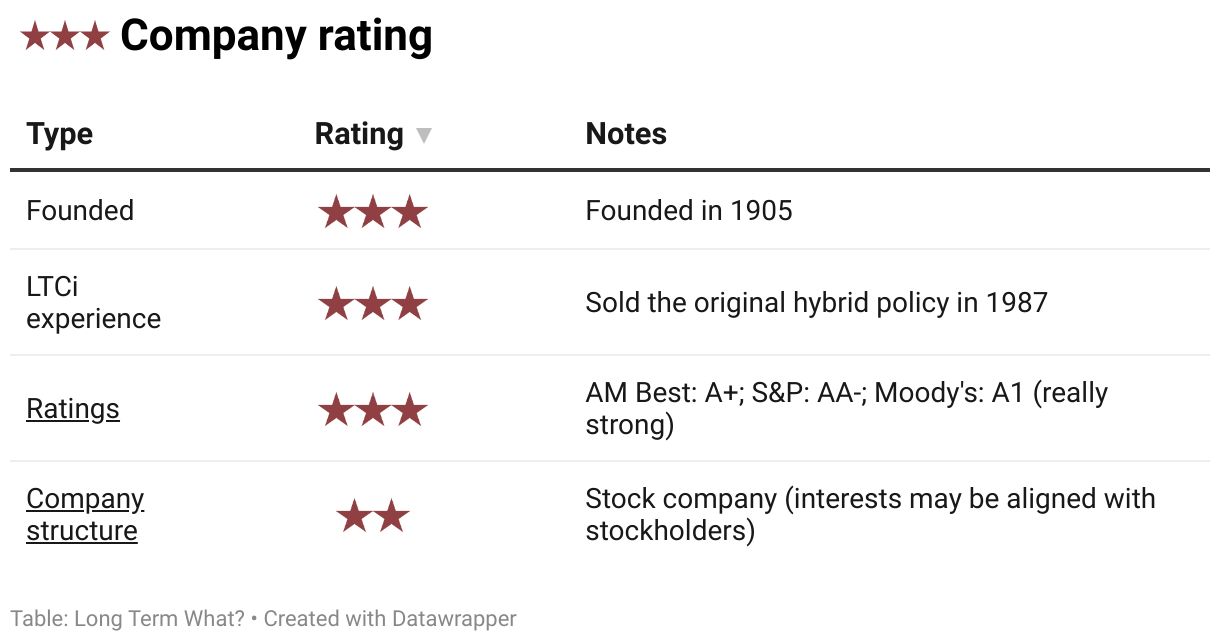

Company

Choose a top-rated insurer for reliable LTC coverage. We work only with financially strong companies to ensure they’ll be there when it counts.

Lincoln has a long history and strong ratings, but as a stock company, its decisions may prioritize shareholders.

Comparisons

How does this policy stack up against others? Focus on what matters most to you to find the best fit.

Benefit pools

Below is a comparison of benefit pools for the same premium. Benefit pools are just one of several factors to consider when evaluating LTCi policies.

Benefits

In this table, you can compare the benefits of all the LTCi policies we offer. You can:

- Search for any detail.

- Tap any column title to sort.

- Scroll right to view more columns. ➡️

Next steps

If this policy seems like a good fit, take the quiz below and include 'MoneyGuard Fixed Advantage' in the notes section at the final step.

Wrap up

Since they updated their pricing in 2024, this MoneyGuard policy hits a high note with one of the best benefit pools for the money on the market. However, you'll need to balance this strength with the limits of its reimbursement policy. Like finding the right harmony in a song, comparing multiple policy quotes tailored to your needs will help you find the right fit.