Intro

Brighthouse Financial entered the long-term care insurance (LTCi) market in 2017 with SmartCare, an individual hybrid policy, after spinning off from MetLife.

Competing against industry giants with over a century of experience, Brighthouse lacks their legacy reputation but leans on innovation to stand out:

- Cash indemnity payouts: Spend your benefits however you see fit.

- High benefit pool: Get access to more funds for care costs.

- Benefit growth linked to an index: Enjoy the option for higher growth.

- Great international benefits: Ideal if planning to retire abroad.

- Streamlined underwriting: A faster and simpler approval process.

- High benefits for NY residents: Unlock greater benefit growth potential.

These innovations are a bit like Billy Beane, the Oakland A's general manager, portrayed by Brad Pitt in Moneyball. Facing wealthier, more established rivals, Beane revolutionized baseball by using data-driven analysis to build a competitive team on a tight budget.

This 30-second clip describes his strategy from this fantastic movie:

Brighthouse SmartCare is following a similar playbook—leveraging modern and creative strategies to challenge industry heavyweights.

As you consider your options, let the letters “LTC” guide you: Learn about the choices available, Talk openly with family, and Create a plan that supports your shared future. Like a solid baseball game plan, SmartCare helps you make smart moves to cover your bases.

Post jargon

benefit: the amount LTCi pays for covered care expenses

benefit period: the maximum time LTCi pays for care after criteria are met

benefit pool: total amount available in LTCi for care expenses

cash indemnity: pays the full benefit, regardless of the actual care costs

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

elimination period: the waiting period after criteria are met before benefits start

exclusion: an insurance rule that denies benefits for specific risks

inflation protection: LTCi benefit that adjusts for rising costs

premium: the payment to maintain insurance

rider: an insurance add-on

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

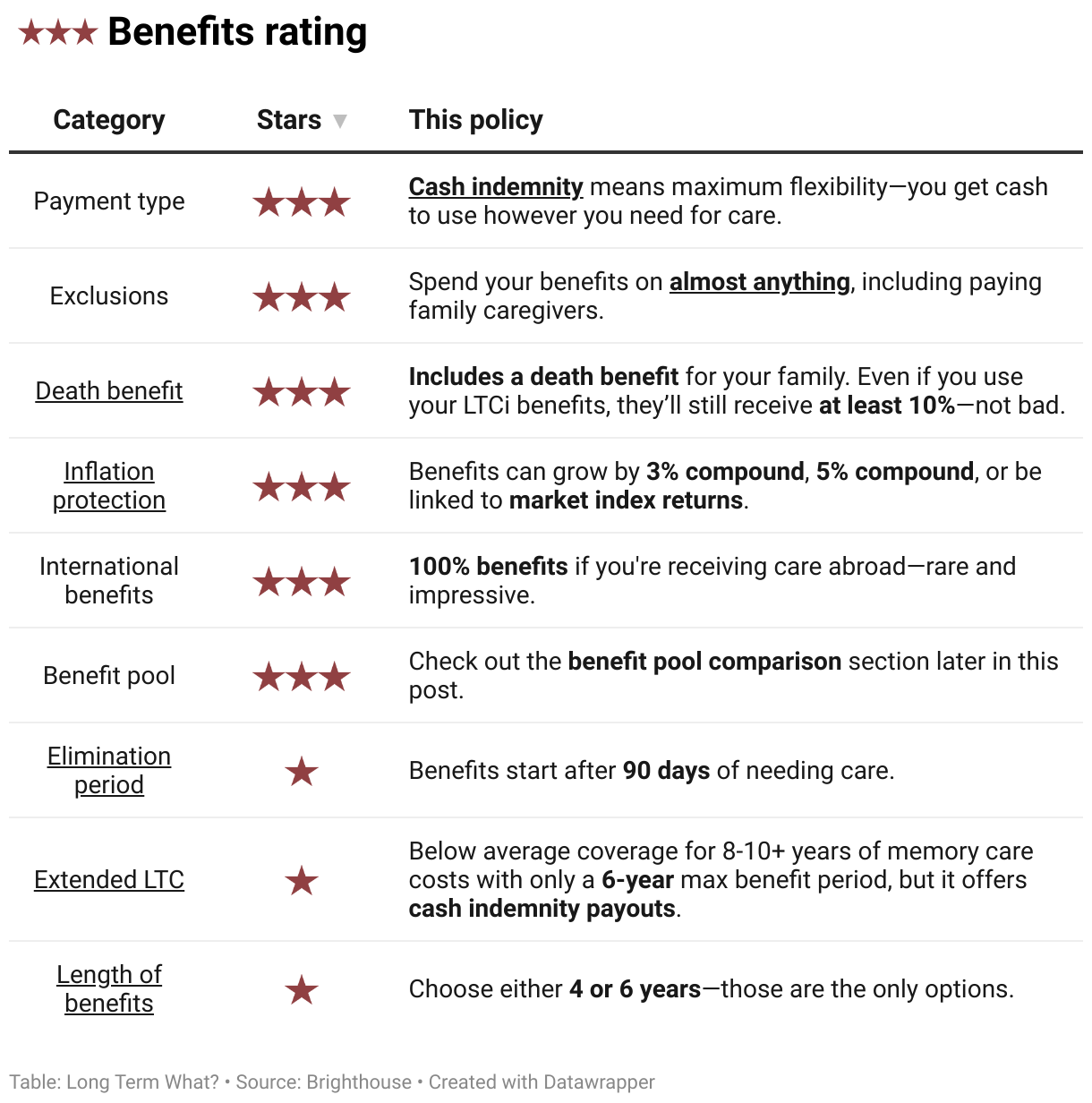

Standard benefits

SmartCare comes with many standard benefits of a hybrid policy:

- Guaranteed premiums: Your costs can never...go...up.

- Guaranteed benefits: Your payouts always match your policy terms (except their Indexed LTC option).

- Benefit triggers: Coverage starts when you need help with two ADLs or cognitive decline.

- Broad coverage: Includes informal care (e.g., family), home health care, adult day care, assisted living, nursing homes, memory care, CCRCs, care coordination, respite care, and hospice.

- Inflation protection (optional): Keeps your benefits aligned with rising costs.

- Death benefit: If you never use your benefits, your family receives a payout upon your death.

- Money-back option: Cancel your policy anytime and get some or all of your money back.

What's special about SmartCare?

In a competitive market, policies often include standout features to set themselves apart. Let’s take a closer look at what makes SmartCare special.

Cash indemnity payouts

This policy offers cash indemnity payouts, providing higher payouts and greater flexibility compared to traditional reimbursement-based policies.

- No need to submit receipts – less paperwork, less hassle.

- Full, maximum benefit – paid each month, regardless of actual care costs.

- Freedom to spend on any type of care – including payments to family caregivers, with fewer exclusions and no approvals required.

High benefit pool

A benefit pool is the total amount available to cover long-term care expenses, whether for home care, assisted living, or other support.

This policy offers one of the largest benefit pools on the market, delivering more value for your premium dollar. At the bottom of this post, you'll find a comparison table showing how it stacks up against other policies.

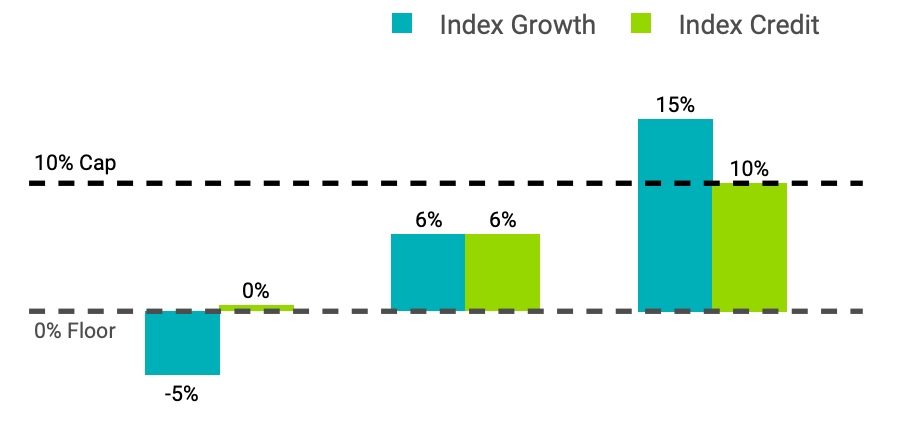

Benefit growth linked to a stock market index

SmartCare offers three options for how your benefits grow over time:

- Level LTC: Your benefits don't grow.

- Fixed Growth LTC: Your benefits grow by 3% or 5% compounded (earn interest on interest).

- Indexed LTC: Your benefits grow based on a stock market index.

Yep, tying your benefit growth to the stock market is different. In most other policies, growth is guaranteed at a fixed rate. With this policy, you can choose non-guaranteed growth tied to a stock market index, like the S&P 500.

How it works

- If the market is negative: Your benefits stay flat (0% growth).

- If the market is positive: Your benefits grow up to a capped percentage (e.g., 10%), called an index credit.

See this chart provided by BrightHouse:

- Ex. 1: The market is down 5%, so your benefit grows by 0%.

- Ex. 2: The market is up 6% (below the cap), so your benefit grows by 6%.

- Ex. 3: The market is up 15% (above the cap), so your benefit grows by 10%, the limit.

At first glance, this policy sounds great—if the market goes up, you win. If it goes down, you don’t lose (0% growth).

Except... it's complicated

But when you dig deeper, things get more nuanced. After years of designing financial products on Wall Street, I’ve learned that complexity usually isn't good for customers.

Here are some things to consider:

- Cap rates change – According to Brighthouse, "Rates are subject to change at the discretion of the issuing insurance company." In short, cap rates can decrease, limiting your potential growth over time.

- Market indexes can underperform – If market returns stay low for years, your benefits may not grow enough to surpass the predictable 3% or 5% guaranteed growth offered by other options.

- Index credits don't include fees – In the Fixed Growth LTC option, 3% means you earn 3%. But in the Indexed LTC option, a 6% index credit is actually 6% minus fees, reducing your net growth.

For a clearer picture, we can help you navigate the dense policy details and better understand the risks involved.

Great international benefits

If you’ve got the travel bug or dream of retiring abroad, it’s important to consider how your long-term care policy will support you internationally. Many countries, like Costa Rica and Thailand, offer high-quality long-term care facilities at a fraction of U.S. prices.

However, most LTC policies provide limited international coverage, often paying only a fraction of your benefits or covering care for a short period. With SmartCare, you’ll receive 100% of your long-term care benefits as a cash indemnity benefit, no matter where in the world you choose to receive care. No borders, no barriers—just the freedom to live (and age) wherever your passport takes you.

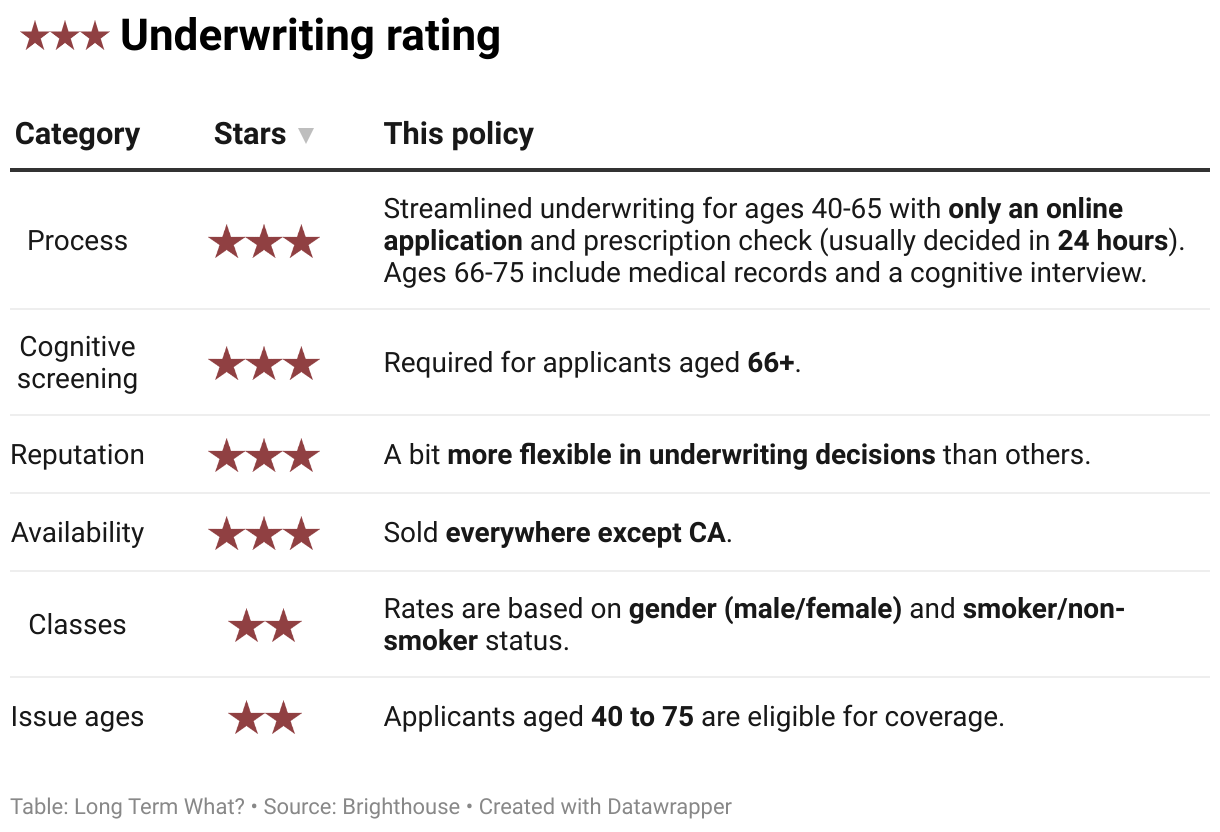

Streamlined underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

Brighthouse promotes its simple, modern, and fast process. For applicants under 65, most only have to complete an online questionnaire, and decisions are usually made within 24 hours.

High benefits for NY residents

Brighthouse SmartCare is one of the few hybrid policies available in New York, offering some of the highest benefits. Unlike others, it provides inflation protection for both the acceleration of benefits (AOB) and extension of benefits (EOB) pools.

Typically, inflation protection only applies to the EOB pool, but with this policy, your benefits grow faster across both pools, giving you more value over time.

In plain English, you get more benefits.

The details

If this policy looks interesting, we’ll dig into the details—because finding a winner often comes down to spotting that one detail that's perfect for you.

We rate each policy’s benefits, premiums, underwriting, and company on a three-star scale, with three stars being the best.

Benefits

Benefits are what the policy pays for covered care expenses.

SmartCare combines key hybrid policy benefits: cash indemnity, minimal exclusions, a death benefit, plus a substantial benefit pool.

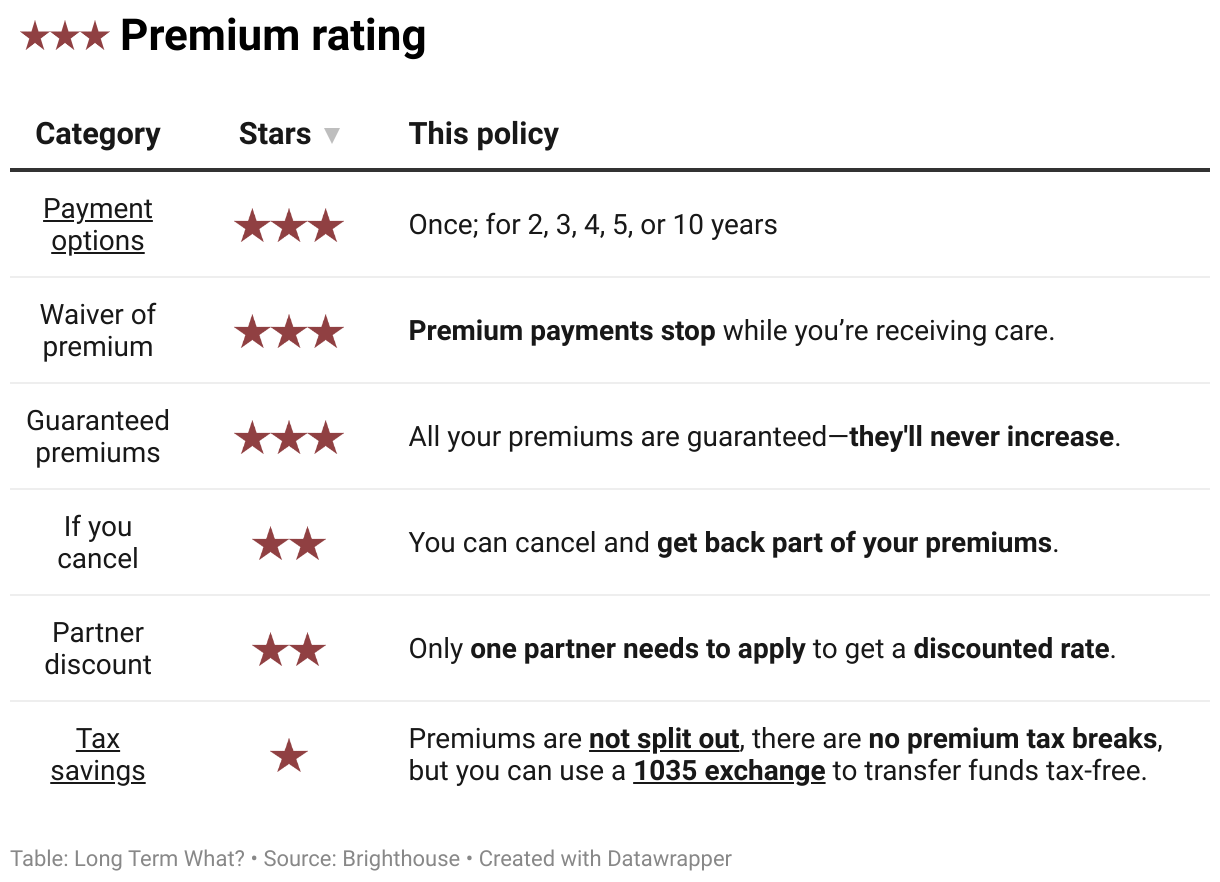

Premium

Premiums are what you pay for insurance coverage.

Brighthouse offers multiple premium options, and the premiums are guaranteed not to increase. However, it doesn’t include any tax advantages.

Underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

BrightHouse offers one of the most streamlined underwriting processes in the industry.

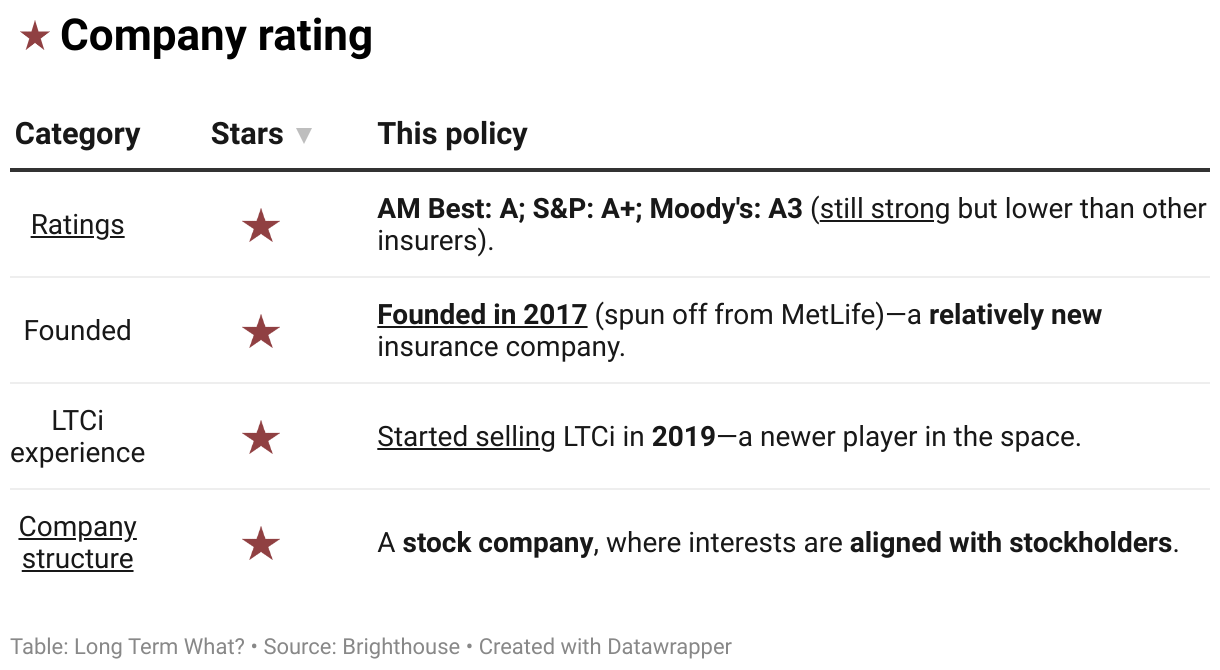

Company

Choose a top-rated insurer for reliable LTC coverage. We work only with financially strong companies to ensure they’ll be there when it counts.

Brighthouse Financial, founded in 2017 as a spin-off from MetLife, is the youngest insurer we offer, but it stands on a strong financial foundation.

Comparisons

How does this policy stack up against others? Focus on what matters most to you to find the best fit.

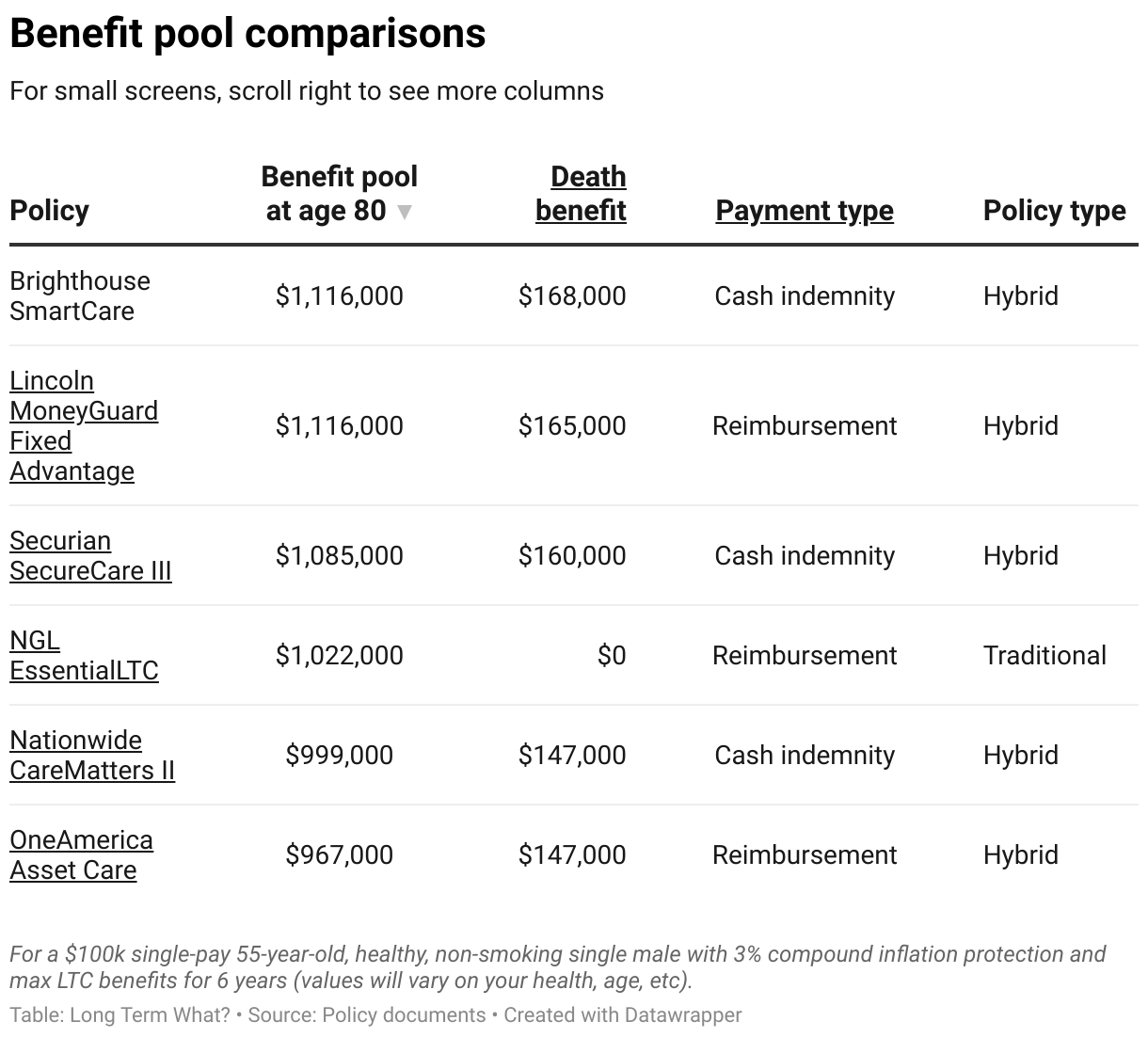

Benefit pools

Below is a comparison of benefit pools for the same premium. Benefit pools are just one of several factors to consider when evaluating LTCi policies.

Benefits

In this table, you can compare the benefits of all the LTCi policies we offer. You can:

- Search for any detail.

- Tap any column title to sort.

- Scroll right to view more columns. ➡️

Next steps

If this policy seems like a good fit, take the quiz below and include 'Brighthouse SmartCare' in the notes section at the final step.

Wrap up

Brighthouse SmartCare is a bold player in the LTCi space—much like Billy Beane and his Oakland A's, they're leveraging unconventional strategies to compete against industry giants.

- Their Fixed Growth LTC option offers a robust benefit pool, excellent international coverage, and streamlined underwriting, making it a strong choice for many.

- Meanwhile, their Indexed LTC option introduces a more innovative—but riskier—approach to benefit growth.

If you value innovation and are open to working with a newer insurance company, SmartCare could be a great fit. However, if you prefer the stability of a more established provider, other policies might better suit your needs.

Either way, we’re here to help you analyze the playbook and decide if SmartCare fits your long-term care strategy.